The good news may be in the past, and now is the time for airlines to digitize and reassess their competitive positions.

What a difference a couple of years can make. In 2013, Warren Buffett called the commercial aviation industry a “death trap for investors.” In 2016, the legendary value investor spent more than US$1.3 billion buying the stock of four major U.S. commercial carriers: American Airlines, Delta, United Continental, and Southwest Airlines — and he has recently upped his stake to more than $8 billion.

Notwithstanding the speculation that this action is a precursor to Buffett’s company, Berkshire Hathaway, taking one of these major carriers private, Buffett seems to be betting that consolidation will continue to pay off for the airlines. He may or may not be right, but it is undeniable that airlines in the U.S. and in most other regions are enjoying a run of good results, buoyed by steadily rising demand and an extended drop in fuel costs. Industry-wide passenger traffic grew by 6.3 percent in 2016. And according to the latest International Air Transport Association (IATA) figures, commercial airlines posted their strongest financial performance ever in 2016 — reporting $35.6 billion in net profit, just a bit above 2015 results but nearly double those of 2014. For the third consecutive year (and only the third year in airline industry history), carriers reported a positive return on invested capital.

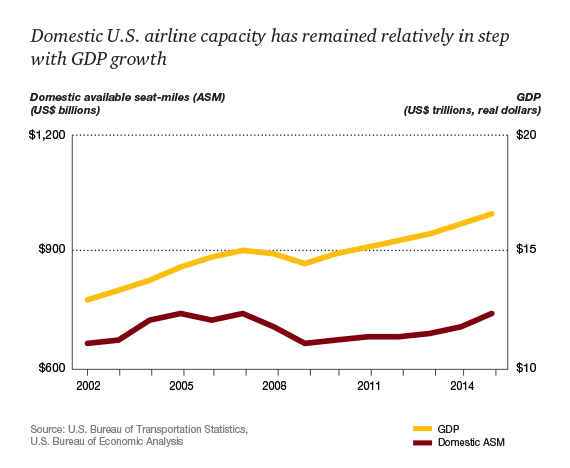

If you are an airline executive, the rising fortunes of your businesses are welcome news — but you know that big challenges remain. Several trends hint that this year and beyond could be problematic. Oil prices are increasing, and global traffic growth is expected to slow in 2017, according to the IATA — a slowdown that is particularly likely if GDP growth remains sluggish. Both trends would make it harder for the industry to maintain recent high levels of profit per passenger. Indeed, to ensure long-term prosperity, a sense of urgency is required now; figuring out how best to exploit the financial headroom you’ve just attained should be at the top of your strategic agenda.

As we talk with airline executives around the world, we find that they are fully engaged in this pursuit. They know that current conditions have not come about because the industry has resolved its structural issues — falling ticket prices, for example, are still a challenge — and that the results they are enjoying now will inevitably attract heightened competition and new players. Witness Norwegian Air’s successful effort to gain permission to fly into the United States. Airline executives also are aware that they need new and more resilient strategies. In our view, two essential drivers of these strategies will be the use of digital technologies and the development of sharper, more nuanced competitive positioning.

dilemma

Digitization is top-of-mind throughout the commercial airline industry, but moving beyond buzzwords like AI and IoT to actual applications can be difficult. Rather than getting bogged down in the “shiny object” aspect of technology trends, think more practically: Specifically, think in business terms about what digital technologies enable; what opportunities they offer to grow the top line and reduce operating costs simultaneously.

Airlines, airports, and direct-to-consumer distributors — travel and lodging providers such as TripAdvisor, Google, and Airbnb, which recently announced its plan to expand beyond lodging and begin offering “experiences” — are all vying for pieces of business or recreational passenger budgets. The technology companies have an advantage in this battle: Consumers like the convenience of one-stop shopping on seamless digital platforms.

To capture top-line growth in this competitive environment, airlines need to incorporate the best of what these so-called channel consolidators do and offer holistic and attractive travel distribution programs. They need to ensure that their direct distribution channels (primarily websites and phone banks) and loyalty programs can deliver personalized service and offers to business and leisure customers. Simply put, airlines must combat ticket commoditization by developing, alone or in partnership with global distribution systems, enhanced merchandising applications that will allow them to cross-sell and upsell using their privileged access to millions of global travelers.

Carriers cannot afford to focus solely on ticket sales, leaving other companies to pick up the ancillary revenue — including lodging, rental cars, entertainment, and personalized itineraries — that surrounds the flight. Fully embracing this mode will make it more profitable than the half-hearted approaches they have employed up until now, but airlines will have to build extensive digital marketing capabilities, integrating the reams of customer data they collect into a complete view of the traveler, transforming the insights yielded by this data into compelling offers (“We know where you and the kids have stayed at Disney World the past five years; would you like a discounted hotel room there this year?”), and constructing an interface and apps that make them stand out in a crowded market.

At the same time, airlines need to use digitization to enhance and optimize operations — to reduce costs while improving service. They need to put technology to work in predicting and preventing equipment failures, in optimizing processes and productivity on the ground, and in providing better and timelier information to employees.

Airline executives need to also keep in mind that digitization is not a panacea; instead, it is a tool for tactical innovation. Your business strategy — the company’s short- and long-term goals — will point the way to the customers you want to win, the offerings you hope to provide that attract these customers, and the right channels for reaching them. When those objectives are known, you can identify the technologies that best support them.

positioning

The once clear-cut competitive landscape in the commercial airline industry continues to evolve. Low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs) are still gaining market share from the dominant full-service carriers (FSCs). But the differences between the models are shrinking.

The black-and-white version of the no-frills ULCC is starting to go gray, as more and more of these carriers and LCCs offer optional, pay-as-you-go upgraded services to their customers. This hybrid approach is particularly effective in emerging markets where passengers are becoming more sophisticated and demanding in terms of service. Similarly, some FSCs (including United Airlines and American Airlines) are tweaking their models by offering more and more ULCC-like basic services to cater to value-based customer segments. And some carriers are operating separate but clearly segmented airlines under their corporate umbrella. FSCs have established LCCs; for instance, Garuda Indonesia spun off its low-cost Citilink subsidiary in 2012 and Lufthansa created Germanwings and merged it with Eurowings in 2015. Similarly, LCCs have established more upscale airlines, such as one-class Lion Air’s creation of two-class Batik Air in 2013.

This morphing and melding in competitive positioning is driven by the varied needs of the market’s customer tiers, by the market’s maturity, by the level of market consolidation, and by the ability of an airline to satisfy expectations within a market better than its competitors. Making an assessment of the market is a complex undertaking that will produce wildly different results by region. In the U.S., a wave of consolidation has yielded fewer and larger airlines, and that seems to be enforcing more discipline concerning fare levels and capacity expansion. In Europe, the competitive field remains fragmented; major European airlines are facing stiff competition from local LCCs and now some Middle East airlines (including Emirates, Etihad Airways, and Qatar Airways). As a result, European airlines are shedding volume on Europe–Asia routes while yields on intra-Europe flights are shrinking. In China and Southeast Asia, LCCs that serve new flyers are still ascendant, but they are moving into hybrid model territory in response to the emergence of more experienced and thus more demanding customers, who want better service and are willing to pay a bit more for it.

As an airline executive, once you have chosen the most potentially lucrative competitive position by market, you must consider how to best construct the business that will inhabit it. Does your airline have the elements — that is, network, fleet, operating model, a reasonable cost-to-serve structure, digital capabilities, and the right partners — needed to thrive in the envisioned business environment? If not, how will those elements be obtained — through organic growth, consolidation, M&A, or joint ventures?

The best answer to this question will depend on the market. In North America, for instance, M&A has been a beneficial option for incumbent airlines. Conversely, in Southeast Asia, where regulations discourage the presence of non-national airlines, alliances may be the best way to serve the regional market.

The need to address competitive positioning is made more serious by the fact that no market is safe from competitive threat. Massive investments in infrastructure in the Middle East (and expansion by the Gulf carriers) will ensure that the region continues to develop as a travel hub connecting the East and the West. Although China’s airlines are still focused on domestic demand, inevitably they will turn their attention outward — bringing huge fleets and large amounts of capital with them.

In response, American and European airlines will not only need to defend their home markets, but also need to more aggressively consider how to enter emerging markets. Making equity investments in emerging markets is a particularly good way of achieving the latter goal. Such investments can give airlines a seat at the table in growth markets with high barriers to entry and position them as preferred partners in the expansion plans of the airlines in which they invest. Most important, these equity investments buy the means with which to build a flexible global airline strategy and align with a business model that seeks to maximize returns from profitable routes while expanding into emerging regions and getting a piece of the revenue as international travel patterns evolve.

There is an urgency attached to making equity investments, because the opportunities are limited and early movers are already acting. Last summer, Qatar Airways boosted the stake it had in British Airways owner International Airlines Group to more than 20 percent. Meanwhile, Delta has filled gaps in its global network with stakes in Virgin Atlantic, China Eastern, Aeromexico, and Brazil's GOL. But although this strategy can help in prying open new markets or cementing a presence in a region, carriers must be careful to make the right decisions about who to partner with and must be certain that they can afford the integration costs. United Arab Emirates’ Etihad Airways, for example, acquired major stakes in European players such as Alitalia, Air Serbia, and Air Berlin but is now considering pulling back on this strategy. Etihad’s position has been weakened by overexposure to losses in these European investments.